Strategic choices for the 2030s writes Kate Davidson of Athena Strategic Thinking Ltd.

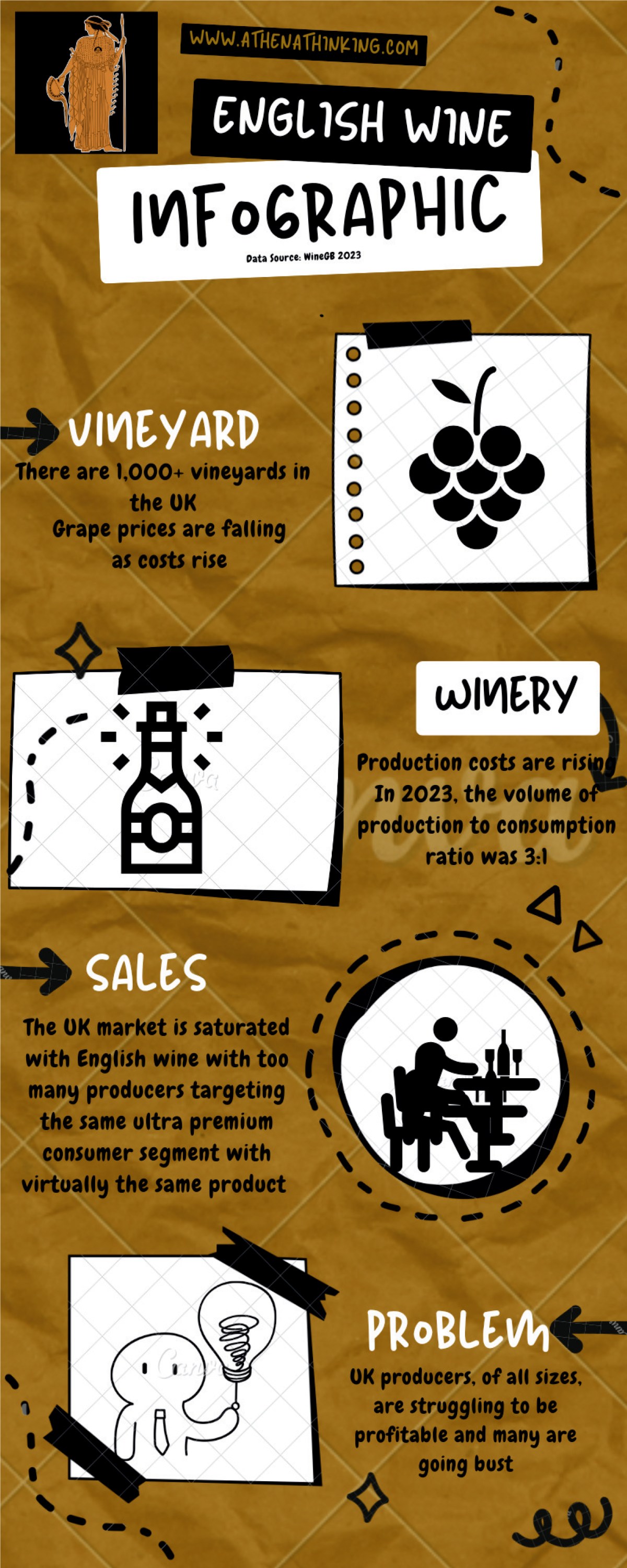

English wine enters the second half of the 2020s in a paradoxical position. Quality is deemed high, global recognition is growing, and investment continues to flow into vineyards and production. Yet beneath this progress sits a more fragile reality: market relevance and demand are not keeping pace with supply or ambition.

This research, conducted by Athena Strategic Thinking, set out to understand where English wine stands today, and what must change to secure its future into the 2030s.

Understanding the market English wine is actually competing in

The UK drinks market is diverse, crowded and increasingly value-driven. Wine competes not just with other wine categories, but with beer, spirits, low-alcohol and no-alcohol alternatives and experience-led consumption. Against this backdrop, English wine occupies an ambiguous space.

Consumers are aware of it, but struggle to define it. Buyers recognise its quality, but face barriers around price, consistency, volume and ease of access. Producers hold differing views on whether the category should focus on premium positioning, affordability, sustainability, localism or innovation.

The absence of a clear, shared identity weakens the category’s ability to convert interest into loyalty.

Consumer behaviour is fast changing

Primary consumer research revealed a widening gap between how English wine is perceived and how people make decisions when buying alcohol.

While consumers express strong values around sustainability, local provenance and national pride, purchasing decisions are still dominated by price, accessibility and occasion fit. Wine consumption overall is declining, particularly among younger adults, who are more selective, health-conscious and experience-driven.

This presents both a threat and an opportunity. English wine can no longer rely solely on heritage-style narratives or technical prestige alone. It must compete for relevance in moments that matter to consumers’ lives.

The missing link: customer understanding. “Awareness is not the problem. Conversion to trial and repeat purchase is.”

Across consumer surveys, buyer interviews and producer focus groups, one issue consistently surfaced: the knowledge gap between producers and consumers.

Consumers lack confidence navigating the category and perceive risk in buying an expensive product which may not be recognised by others; many producers lack robust, evidence-led customer insight to guide pricing, range architecture, communication and experience design. This limits demand and reinforces the perception of English wine as “special occasion only”.

If producers knew their customers as well as they know their soil, the category’s growth trajectory would look very different.

Eight strategic challenges for the 2030s

The research identified eight strategic challenges that will shape English wine’s future:

- Developing the identity of English wine

- Building an effective marketing funnel

- Closing the producer–consumer knowledge gap

- Adapting to demographic change and declining consumption

- Broadening the product range into affordable premium

- Positioning vineyards as experience-led memory makers

- Addressing the value–action gap

- Restoring industry equilibrium through scale, focus and collaboration

Two challenges stand out as particularly urgent.

First, price and access. The current price positioning excludes most UK wine drinkers. Growth will require credible offerings below £20 that protect quality while unlocking the mass-affluent market.

Second, structural balance. Supply is outpacing demand. Larger producers face pressure to scale, consolidate, export and reduce costs, while smaller producers must lean into premium positioning, direct-to-consumer routes and distinctive experiences. As the market polarises to niche and large players, the middle ground becomes a tricky spot for producers. “Supply is growing faster than demand and structural imbalance is becoming harder to ignore.”

A strategic choice, not an inevitability

The future of English wine is not pre-determined. If the industry fails to align with evolving consumer behaviours and expectations it risks stagnation, admired, but increasingly marginal. However, those producers who reimagine their proposition, manage costs actively, invest in experience and storytelling, and collaborate at local and national levels stand to shape a new era of sustainable growth. “The next decade will not be defined by who makes the best wine, but by who builds the strongest connection with the people drinking it.”

This research was never intended to sit on a shelf. It forms a strategic toolkit designed to support informed decision-making, from individual business workshops to regional collaboration and national strategy development.

The question now facing the industry is simple but uncomfortable: will English wine shape its future deliberately or allow the market to decide it for us? Key findings are now available along with a full report and workshop facilitation.